Unsure how these changes will affect your current or potential business in Singapore?

Speak to our Tax & Accounting team today to discuss what this means for you.

The $4.0 billion Stabilisation and Support Package was introduced in the Singapore Budget 2020 to provide assurance and support to workers and enterprises in this time of economic uncertainty. In addition to providing cash flow support, the Package supports firms to retain and retrain workers, and share productivity gains with them. Sectors more directly affected by the COVID-19 outbreak will receive additional support.

Budget 2020: Stabilisation and Support Package

On the 26th of March, the Government released a supplemental budget, to address the impact of Covid-19 on the Singapore economy and population. The new budget, known as Resilience Budget, will help employers to address cash flow issues while retaining their employees and it will also allow the employees to defer income tax payments

The main measures that have been released can be summarized as follows:

As of now, for the purpose of this article, we will only focus on the first 4 measures that we believe will have a greater and direct impact on our clients’ business and operation

The Jobs Support Scheme (JSS) will help enterprises retain their local employees during this period of uncertainty. It is a temporary scheme for 2020. All active employers, except for Government organizations (local and foreign) and representative offices, are eligible for the JSS.

After the first release, the Jobs Support Scheme has been enhanced, as follows:

Please note employers do not need to apply for the JSS. The grant will be calculated and based on their CPF contribution data.

Table 1: Illustration of Jobs Support Scheme computation

|

|

Months Covered |

Cash grant |

Payments schedule |

|

Tranche 1 |

Oct- Dec 2019 |

25% of the first 4600 SGD of the gross monthly wages per local employees

|

31st of May 2020 |

|

Tranche 2 |

Feb - Apr 2020 |

31st of July 2020 |

|

|

Tranche 3 |

May - July 2020 |

31st of October 2020 |

The JSS payout will be credited to the employers' GIRO bank account used for Income Tax/GST.

For companies that do not have a GIRO accounts, the JSS payout will be paid:

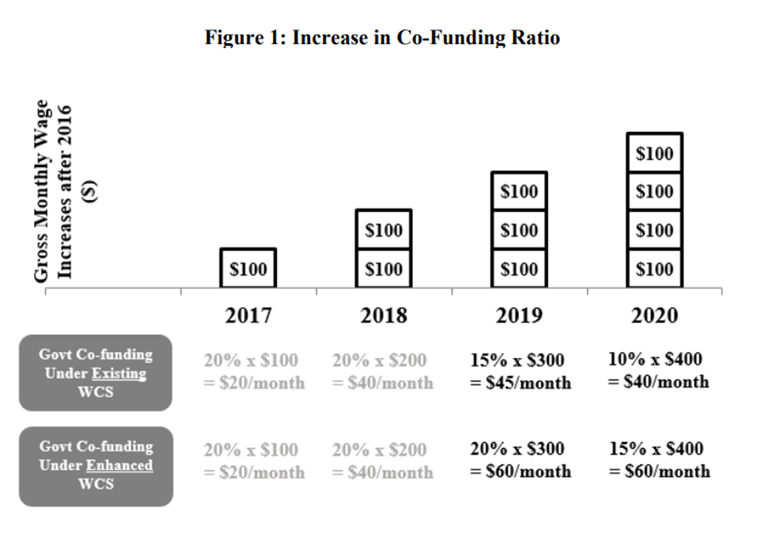

The Wage Credit Scheme (WCS) will be enhanced in the Singapore Budget 2020. WCS supports enterprises embarking on transformation efforts and encourages employers to share productivity gains with workers, by co-funding wage increases.

A summary of the changes to WCS is in Table 2 below.

Table 2: Summary of Changes to WCS

|

Scheme |

Existing WCS |

Enhanced WCS |

|

Qualifying years2 |

|

|

|

Level of co-funding |

|

|

|

Gross monthly wage ceiling |

|

|

|

Qualifying wage increases |

|

|

Employers do not need to apply for WCS.

Illustration of Wage Credit Computation

Raising of Government Co-Funding Ratio

Raising of Gross Monthly Wage Ceiling

Support for companies

Automatic Deferment of Corporate Income Tax (CIT) Payments

All companies with CIT payments due in the months of April, May and June 2020 will be granted an automatic three-month deferment of these payments.

The CIT payments that are deferred from April, May and June 2020 will be collected in July, August and September 2020 respectively.

Companies can expect to receive a letter from IRAS by 15 April 2020.

Support for Employees

Some taxpayers who have filed their Income Tax Returns for Year of Assessment (YA) 2020 would have received their electronic Notice of Assessment (i.e. eNOA or tax bill).

A. Apply to Defer Tax Payment (GIRO)

Taxpayers who have filed their Income Tax Returns for Year of Assessment (YA) 2020 may opt to defer the income tax payments due in May, June and July 2020.

For those employees paying by GIRO, there will be no GIRO deduction in May, June and July 2020. The income tax deduction will resume in August, September or October 2020 and the end-date of the instalment plan will be extended by 3 months.

Employees who wants to benefit from this option must sign up by 31 July 2020.

B. Apply to Defer Tax Payment (Lump Sum Payment)

In case of lump sum payment, the taxpayers may opt to defer the payment by three months.

As part of the Resilience Budget announced on 26 Mar 2020, qualifying non-residential properties (“qualifying properties”) will be granted property tax rebate for the period of 1 Jan 2020 to 31 Dec 2020. This is an enhancement of the property tax rebate announced at Budget 2020, on 18 Feb 2020.

The property tax rebate is enhanced by extending the rebate to additional types of properties, and increasing the amount of rebate for certain types of properties.

Landlords are expected to fully pass on the rebate to their tenants, by reducing rentals, to directly ease the cash flow and cost pressures faced by tenants. For properties that are eligible for 100% property tax rebate, this is equivalent to more than one month’s rental.

Under the Resilience Budget, owners of qualifying properties will be granted rebates of up to 100% on their property tax payable.

The rebate is 100% of the property tax payable for:

The rebate is 60% of the property tax payable for:

The above 100% property tax rebate does not apply to them.

The rebate is 30% for any premises excluding the following:

For avoidance of doubt, no rebate shall be given to vacant land or land under redevelopment.

IRAS will inform owners of qualifying properties on their property tax rebates by 31 May 2020. Owners are not required to submit any claims for the rebate. Owners of qualifying properties can expect to receive their refunds by 30 Jun 2020.

For properties that qualify for 100% rebate, the property tax payable for 2020 will be fully refunded.

For owners who have an ongoing GIRO instalment plan, there will be no GIRO deduction from Apr to Dec 2020. However, if you have tax arrears, the GIRO deduction will resume in Jun 2020.

If owners of properties which are granted 60% or 30% rebate have an ongoing instalment plan, with the rebate offsetting the instalment payment, there will be no GIRO deduction for a period ranging from four to seven months starting from May 2020.

Speak to our Tax & Accounting team today to discuss what this means for you.

Back to top